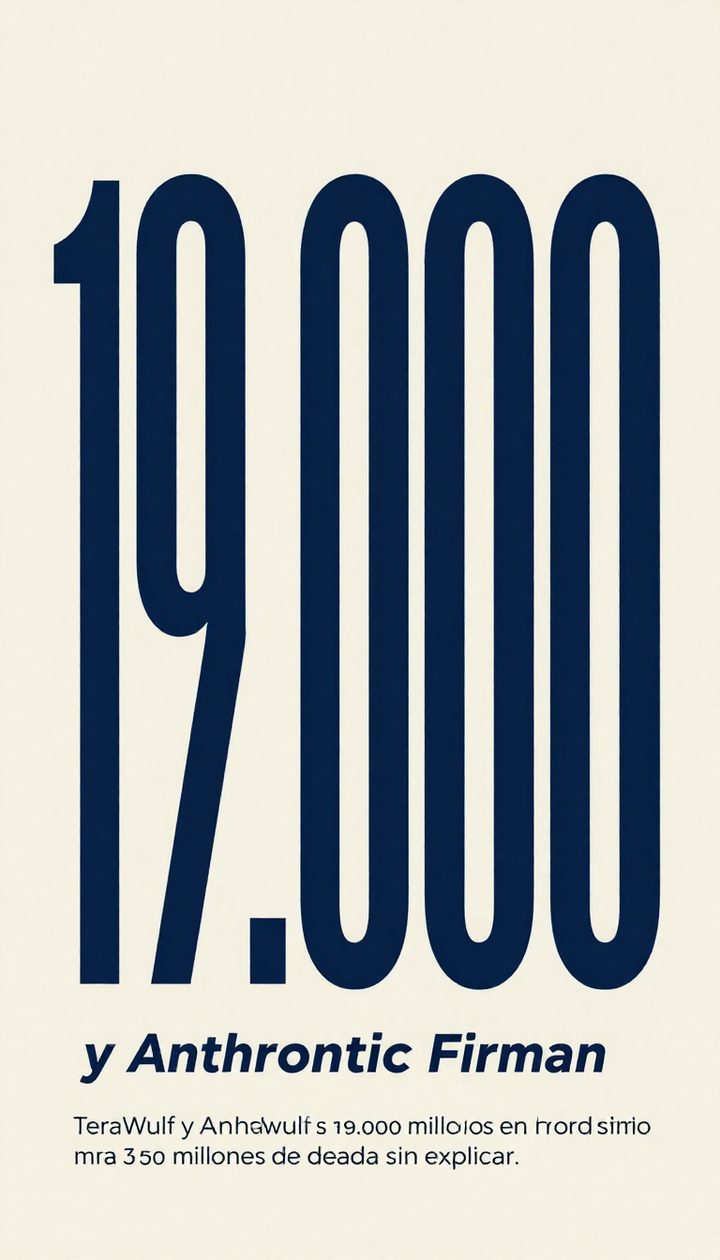

TeraWulf and Anthropic sign $19 billion in compute, but the market eyes the unexplained $3.5 billion in debt

🕒 Published on Zendoric: July 13, 2026 · 00:21

TeraWulf closed a 20-year, $19 billion data center lease with Anthropic, at a price per megawatt 27% higher than its previous contracts. The market, however, punished the stock over the high-risk debt needed to build it.

📚 Go deeper

The reference manual for building products on top of AI models: prompts, RAG, fine-tuning, agents, evaluation and deployment.

As an Amazon Associate, Zendoric earns from qualifying purchases; the price does not change for you. · all our recommended books →

By TS2.tech · July 12, 2026.

TeraWulf (NASDAQ: WULF), until recently a bitcoin miner reinvented as a data center provider, announced a compute lease contract with Anthropic valued at 19 billion dollars over twenty years. The deal covers 401 megawatts of "critical IT load" that will begin generating revenue between late 2027 and early 2028. The figure that has unsettled investors is not the size of the contract, but a 3.5 billion debt package the company has not broken down: according to its CFO, Patrick Fleury, it will combine a leveraged loan with high-yield bonds—debt rated below investment grade and therefore more expensive—led by Morgan Stanley. The result on the stock market was a sawtooth week: a high of 25.15 dollars on Monday, a 8.9% drop on Tuesday, a 12.8% rise on Wednesday and a weekly close of barely 3.7% above the previous level, with a 5.3% plunge on Friday.

The numbers, however, back part of the initial enthusiasm. Doing the simple math—contracted revenue divided by term and capacity—the contract with Anthropic implies about 2.37 million dollars per megawatt-year, versus the 1.86 million TeraWulf earns from its Lake Mariner agreement with Fluidstack: a revenue-density premium of 27%. That figure does not guarantee higher margins—the operating terms and the allocation of services may vary—but it supports CEO Paul Prager's statement that "you can't create megawatts overnight": the shortage of power and construction capacity, not demand, is today the bottleneck that sets the price. The leap in scale is dramatic for a company that in the first quarter billed 34 million dollars across high-performance computing and bitcoin mining: the Anthropic contract, at 950 million a year, is equivalent to seven times that quarterly pace on an annualized basis, before accounting for costs, financing or execution risks.

That is where the market's true test lies. If the new 3.5 billion in debt is placed on terms similar to TeraWulf's previous issuances—coupons of 7.25% to 7.75%—the annual interest cost would be somewhere between 254 and 271 million dollars, that is, between 27% and 29% of the average gross revenue the lease to Anthropic will bring in. Any delay in construction, rise in the cost of electrical equipment or shortage of power would push back revenue while interest keeps running, and would force TeraWulf to choose between more expensive debt or a capital increase that dilutes current shareholders. It is not a hypothetical risk: the company itself has flagged it as its main open front, along with the credit backing that the Kentucky structure requires.

Our reading is that this contract is a symptom, not an anecdote. Behind every "generative AI" headline there is now a financing chain that resembles the construction of energy infrastructure more than software: labs like Anthropic outsource the risk of building megawatts to specialized operators, which in turn pass it on to high-yield debt markets, which in turn bet that demand for compute will keep growing for two decades. It is a chain that works as long as interest rates do not spike and demand for inference does not cool; and it fails, with real pain for shareholders and creditors, if either of those two assumptions breaks. The divergent behavior of comparables such as IREN (+6% on the week) versus Applied Digital (-5.8%) shows that the market is already beginning to distinguish between who builds with solid margins and who is simply adding leverage.

In the long term, however, this type of contract is precisely the kind of physical investment that supports the underlying thesis: without megawatts there are no more capable models, and without more capable models there is no leap toward the abundance—scientific, medical, economic—that we champion as the horizon. The current transition is hard and is paid for with expensive debt, potential dilution and stock market volatility; that has to be said plainly. But the shortage of power and compute capacity that makes these contracts expensive today is also the sign that demand for artificial intelligence is structural, not a passing fad. Whoever survives this capital-intensive construction phase—with solid balance sheets and well-structured contracts—will be better positioned when the cost curve of computing begins, as has historically happened with all critical infrastructure, to fall.

📚 Go deeper

The story of NVIDIA and Jensen Huang: how a video-game card company ended up making the most coveted resource on the planet.

The best starting book if you're not technical: a Wharton professor explains how to work WITH AI — when to delegate, when to supervise, when to keep i

As an Amazon Associate, Zendoric earns from qualifying purchases; the price does not change for you. · all our recommended books →

🔗 Related on Zendoric

- A Nobel Laureate Leaves DeepMind for Anthropic — and the Market Treats Talent as the Real Moat · 2026-06-24

- Wall Street tests the AI promise: when two out of every three stocks rise and the index falls anyway · 2026-06-27

- Upwork integrates Claude AI and raises new funding, but the market still hasn't forgiven a 58% drop in 2026 · 2026-06-28